By Jonathan Kemp at BWCI

jonathan.kemp@bwcigroup.com

“a tectonic shift in

insurance accounting”

IFRS 17 Insurance Contracts, a new insurance accounting standard, represents a tectonic shift in insurance accounting. The implementation date of 1 January 2023 means that many companies are now only a few months away from producing their first annual financial statements under the new requirements. For most it will have been, and probably continues to be, a hard slog. Issues to grapple with include:

- Interpreting the standard and wisdom dispensed by the Transition Resource Group

- New data requirements

- Talking stakeholders through the potential impact

- Helping decision makers understand some of the key decisions they need to make

With so much effort being expended, a common reaction is:

“What’s the point of all this?”

The IASB¹ suggests that the new standard will create:

- Better comparability across countries, different types of insurance contracts and across different industries.

- More transparent and useful information, particularly in respect of profitability.

Whilst these might be laudable goals, the reaction from many SME’s² we have talked to is that they perceive little or no added value to their business. In many cases they have been forced to implement IFRS 17 and can only see the costs incurred from having to do so.

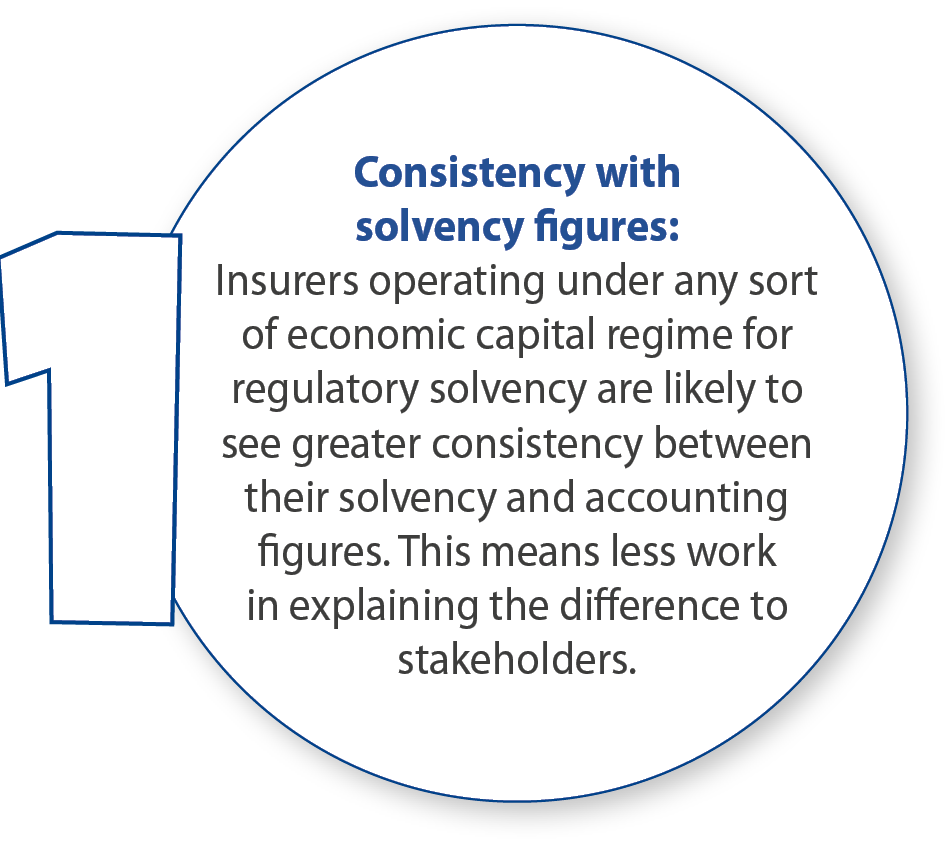

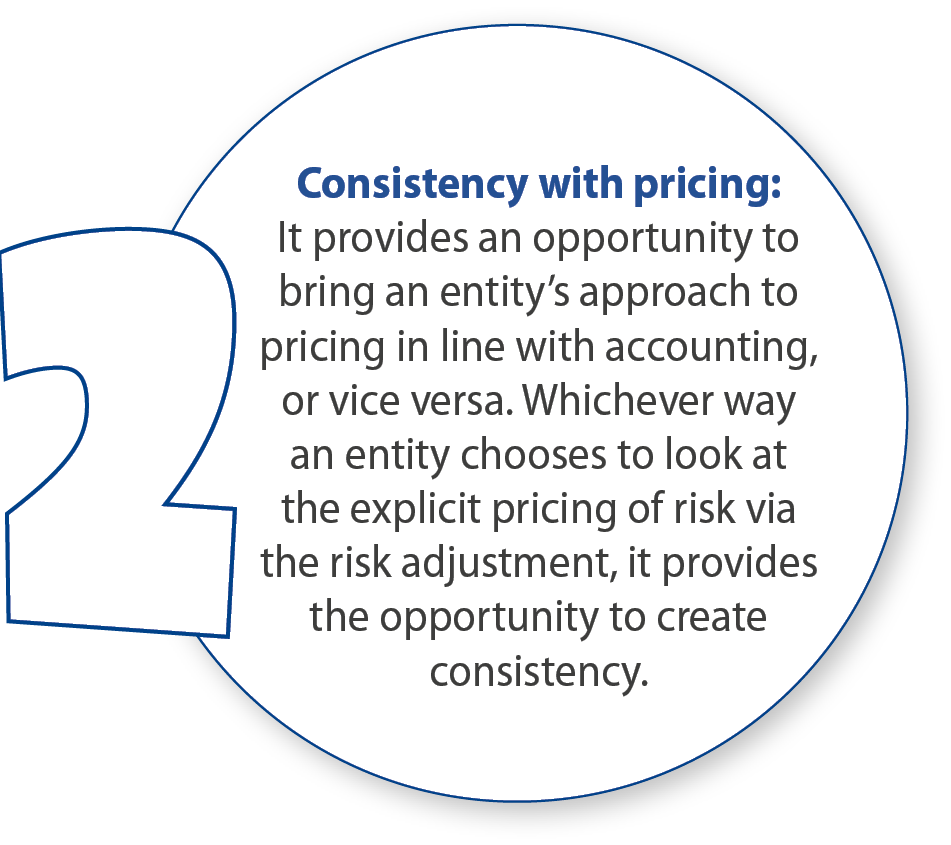

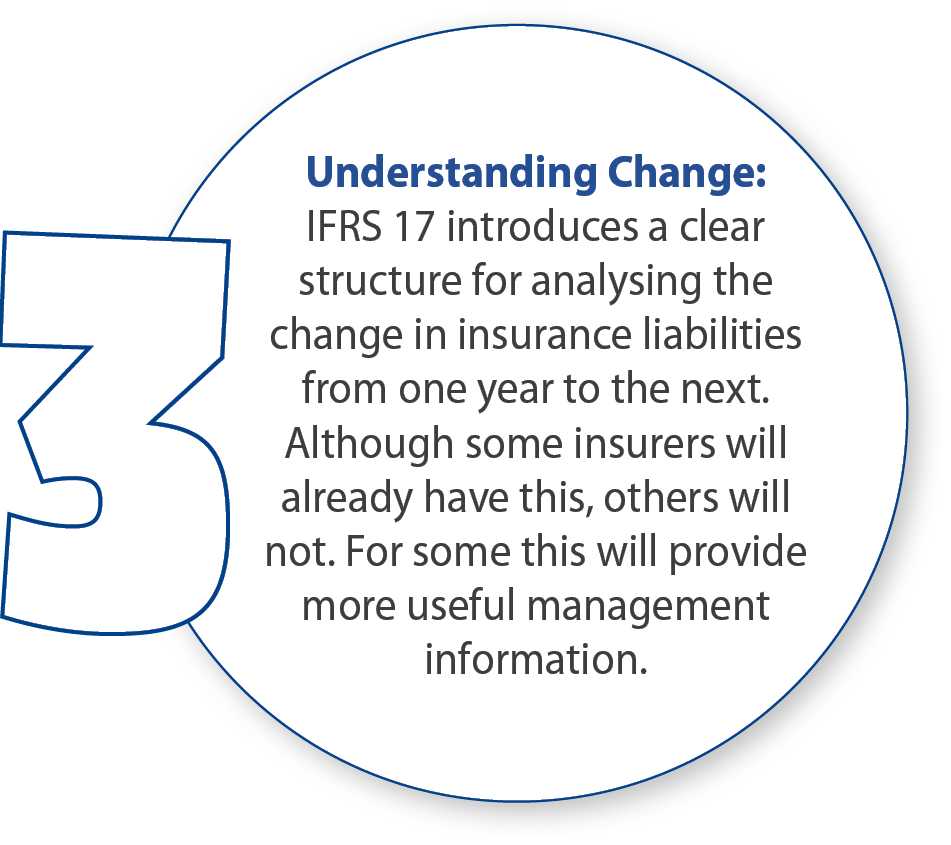

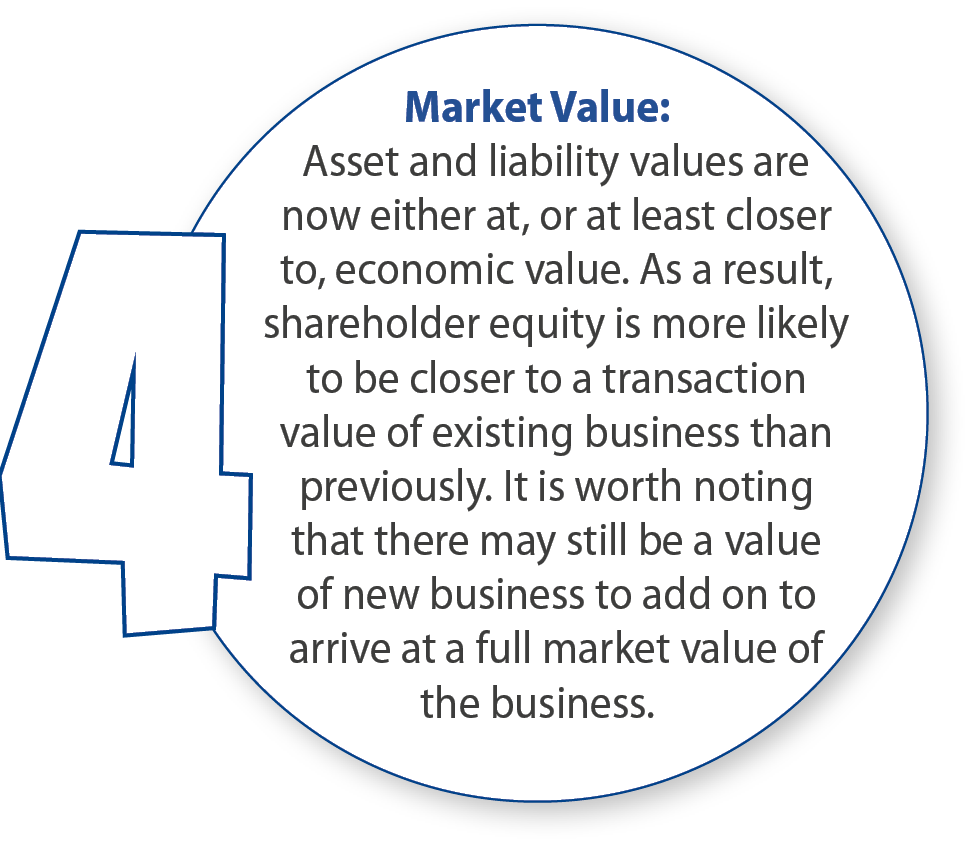

However there are certainly some positives arising from IFRS 17; here are our top 5 reasons to be happy about implementing it!

So even if companies have been “forced” into adopting IFRS 17 and the IASB’s reasoning for the new standard means little to their business, there are almost certainly some upsides.

¹ International Accounting Standards Board ² Small and medium-sized enterprises