By Mike Freer at BWCI

mike.freer@bwcigroup.com

Guernsey’s Secondary Pensions system is edging closer to being launched. After the States debate was unexpectedly deferred for 6 months from May to November last year, a draft of the Secondary Pensions law¹ was finally debated and agreed at the end of 2022. This was followed by an announcement in March 2023 that the legislation will come into force from 1 July 2024. However, only employers with 26 or more staff will need to comply initially.

The draft law contains some helpful details for employers planning what action they need to take to prepare for the introduction of Secondary Pensions in Guernsey. In particular, it covers:

- which employees will fall within scope

- the minimum criteria schemes will need to meet to comply

- the information that schemes must provide to members

- definitions of a number of technical terms used within the legislation

- the Director of Revenue Services’ enforcement powers

- the penalties for non-compliance

What it means for employers

Guernsey’s 2,000 or so employers will be required to automatically enrol “designated employees” into an “approbated pension scheme”. This could be either the employer’s own scheme or the new trust arrangement to be set up by the States.

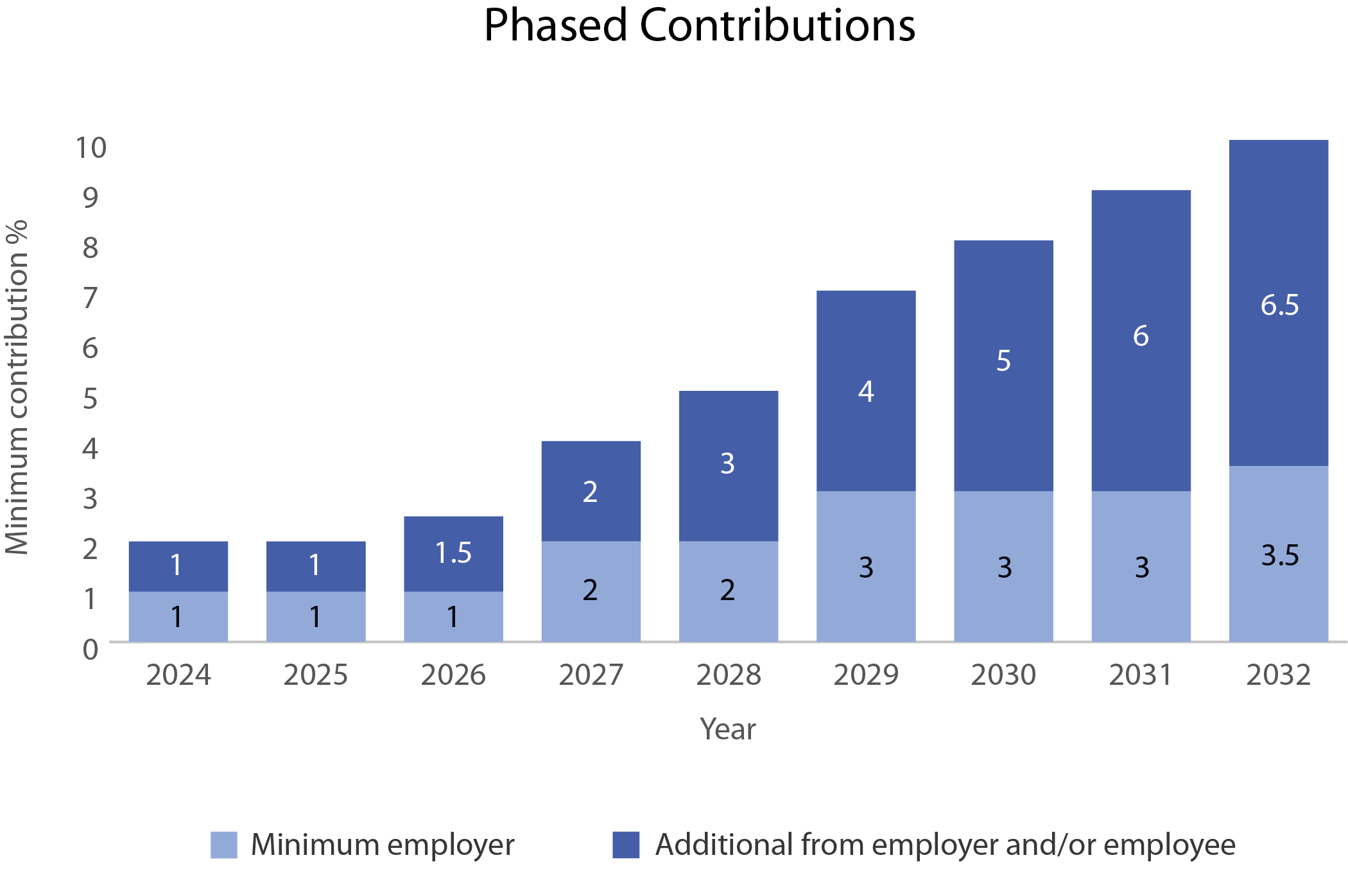

Both employers and employees will be required to contribute, unless an employee has chosen to opt out. The long-term contribution rates will be 3.5% of applicable gross earnings² for the employer and 6.5% for the employee.

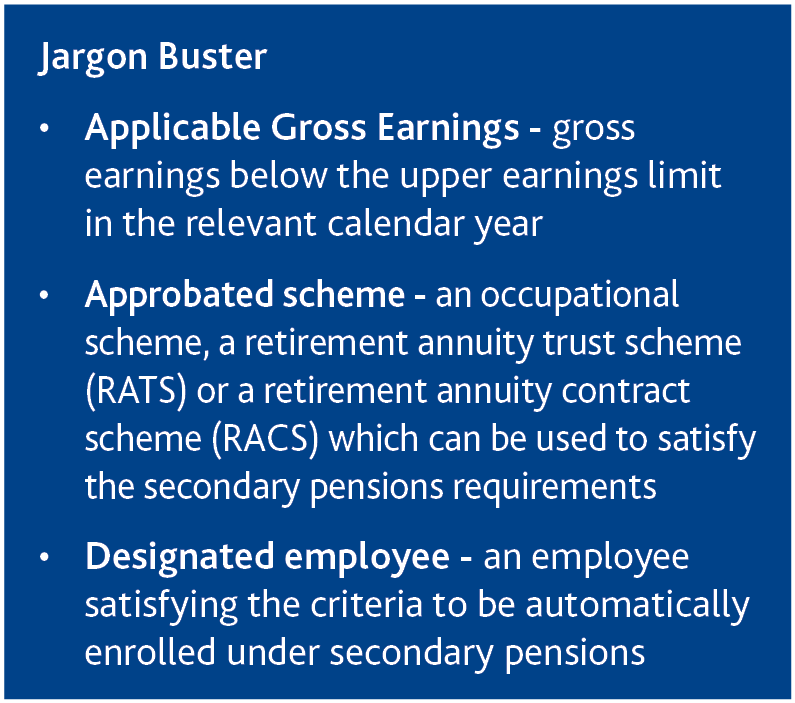

Designated Employees

These are employees satisfying all of the following:

- resident in Guernsey, Herm, Jethou or Alderney

- 16 years old or over

- under Pensionable Age³

- likely to earn more than the Lower Earnings Limit (£8,476 pa in 2023) per annum

- not in full-time education

Employees under age 75, who are over Pensionable Age, or in full time education or earning less that the lower earnings limit, will have the right to request to be enrolled into an approbated scheme.

Opt outs

Designated employees will be able to opt out, but will need to be re-enrolled every three years.

Will your scheme comply?

Schemes which satisfy the secondary pensions requirements will be known as “Approbated schemes” and will need to satisfy all of the following conditions:

- approved by the Revenue Service under section 150 or 157A of the Income Tax (Guernsey) Law, 1975

- subject to a regulatory regime in one of the British Islands⁴

- must provide for auto enrolment

- must not require employees to contribute more than 10% of applicable gross earnings

- Defined Contribution arrangements

- the employer must contribute

- the minimum contribution requirements must be met

- Defined Benefit schemes

- an actuary must certify that the benefits are likely to be at least equivalent, for the majority of members, to the benefits from the minimum contributions

- The scheme funding requirements are expected to be adequate to meet the cost of the benefits as they fall due

- RATS

- must be employer-facilitated or

- if established by an employee, an employer has consented to use it

The requirement to be regulated means that, in practice, a Guernsey scheme will need to have either a licensed fiduciary as either the trustee or administrator.

How much will it cost?

Contributions will be based on the same earnings as those on which Social Security contributions are paid ie up to the Upper Earnings Limit (£168,480 in 2023). However, there is a change from the rates previously published as the full rate contributions will be phased in over 8 years, rather than 7. The minimum employer and joint contributions as illustrated in the chart.

Employers can opt to pay more than the minimum rate, provided that the joint employer/employee rate is not less than the minimum required in any particular year.

How employers are getting ready

Employers who already have a pension scheme are checking if it extends to all staff who would be classed as “Designated employees”. They are also reviewing their current definition of pensionable salary. In many cases this will be basic salary, so some changes may be needed to the scheme’s rules.

Employers who do not currently provide a pension are looking at how they will implement secondary pensions and putting their chosen structure in place. They can then start contributions at a time that best suits them. This might be a pay review date, the start of their new financial year or the latest date by which they have to comply.

¹ The Secondary Pensions (Guernsey and Alderney) Law 2022

² Gross earnings below the Upper Earnings Limit

³ which is being increased from 65 to 70 between 2020 and 2049

⁴ Schemes established in Jersey, before the commencement of the legislation, are expected to be exempt