By Michelle Galpin at BWCI

michelle.galpin@bwcigroup.com

“The IOM FSA confirmed that it intends to base the new provisions on the UK funding requirements.”

In Issue 2 2025 of Bandwagon we reported on the Isle of Man Financial Services Authority’s (IOM FSA) consultation on changes to the Retirement Benefits Schemes Act 2000. The proposed update to the pensions legislation focussed on strengthening the regulatory framework surrounding the funding and governance of defined benefit (DB) schemes. 11 consultation responses were received from a variety of industry stakeholders, including pension providers, insurers and legal advisers.

Following detailed analysis of these responses, the IOM FSA published its Feedback Statement on 4 February, together with an “unofficial” draft of the updated legislation. This comprehensive document addresses the concerns raised and either confirms where changes are intended to be made to address those concerns, or provides commentary on why a particular proposal is still to go ahead as originally intended.

What has been confirmed?

- The IOM FSA are committed to ensuring that the regulatory framework will be proportionate, effective and workable in practice

- The primary legislation is intended to be flexible (which it is why it is lacking in specific detail)

- The detailed requirements will be in secondary legislation and will include the provision for exemptions in some areas

- Associated guidance is to be issued, in addition to the secondary legislation

- There will be further consultation on both the secondary legislation and the guidance

- The legislation will be introduced in phases, with the licensing of trustees and administrators the highest priority

Pension scheme accounts

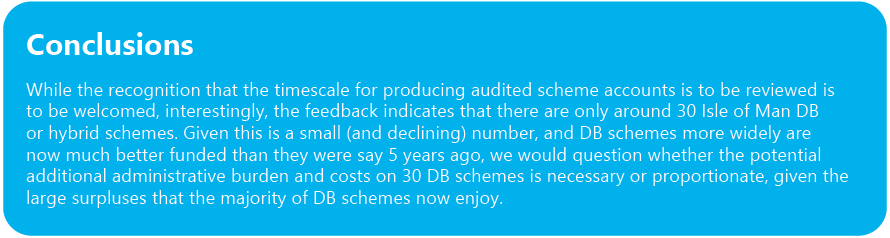

Trustees will be pleased to know that the 6 month deadline for producing audited accounts after the scheme year end is to be amended. In practice, many schemes have struggled to meet this timescale for a variety of reasons; delays in obtaining asset values from third parties and audit capacity are some areas that have been problematic in practice. The time scale will now be prescribed by regulation, although it is not clear what the revised timeframe will be.

Concerns were also raised around the need for scheme accounts to be audited and the feedback confirms that the audit provisions and any exemptions will be considered as part of secondary legislation and will include consultation.

Funding requirements

The feedback document highlights that, at present, there is no statutory framework governing how actuarial valuations are prepared, how deficits are addressed and how schemes should respond to underfunding. It goes on to say that “it understood that most trustees and appointed actuaries have voluntarily followed the UK DB funding standards”, although this has not been our experience.

The IOM FSA confirmed that it intends to base the new provisions on the UK funding requirements. Over 60% of respondents were concerned about the increased costs imposed on schemes from this additional regulatory and compliance burden. The feedback statement indicates that some exemptions may be appropriate and that the framework will be tailored to the local pensions landscape.

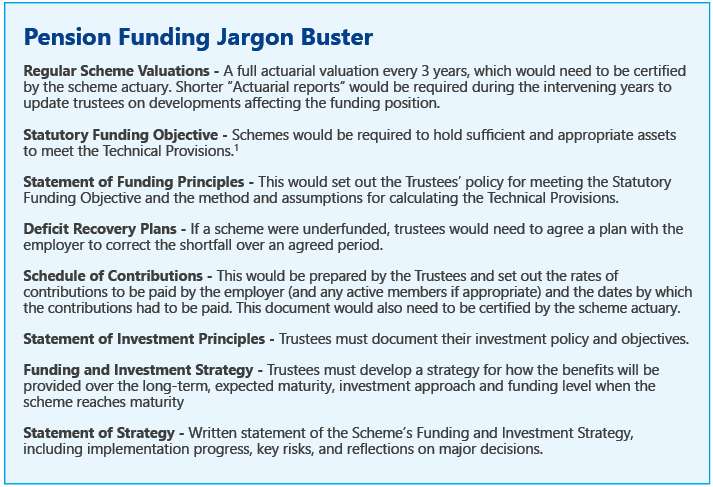

The draft legislation includes a number of new pension terms and we have summarised the key ones below.

¹The Technical Provisions is the amount required (determined by an actuarial calculation) to make provision for a scheme’s liabilities.