By Warwick Helps & Jonathan Kemp at BWCI

warwick.helps@bwcigroup.com & jonathan.kemp@bwcigroup.com

“favouring investment wrappers that offer predictability, flexibility and control over the timing of tax events”

Investment flows into offshore bonds have increased substantially over the last year or so. The Financial Times reported that a record amount of £10.5 billion had been invested over the year to June 2025, up from £5.1 billion the previous year.

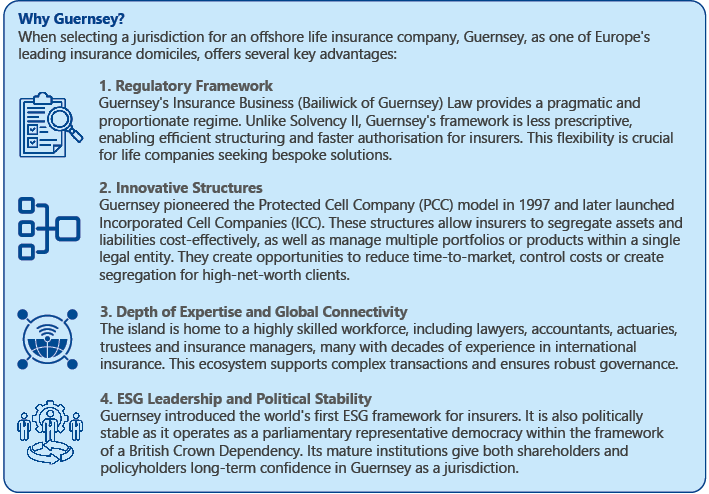

With UK demand for offshore bonds rising, Guernsey stands out as the smart choice for setting up a life insurer, offering pragmatic regulation, innovative structures and deep industry expertise.

What is an Offshore Bond?

An offshore bond is an investment set up by a life insurance company located outside the investor’s home country, typically in a jurisdiction with a favourable tax regime. Investment in these life insurance wrapper products, rather than directly into the underlying assets, may provide an opportunity to defer tax to a favourable time. This is because tax on offshore bonds is not currently paid by UK investors until withdrawal.

Key Drivers

Against the backdrop of continuing fiscal tightening in the UK, offshore bonds have taken on renewed strategic relevance for both advisers and product providers. Successive reductions in tax-free allowances, coupled with higher marginal rates on capital gains and the widening scope of inheritance tax from 2027, are prompting many investors to reassess how and where they hold long-term assets.

This shift is not simply a reaction to short-term policy changes, but reflects a broader trend; UK investors are increasingly favouring investment wrappers that offer predictability, flexibility and control over the timing of tax events. In that environment, offshore bonds are once again being viewed as a financial planning tool, rather than a niche retail product, providing a mechanism to manage crystallisation of gains, smooth income flows in retirement, and structure wealth transfers more efficiently.

A Typical Scenario

Consider a typical high-net-worth client anticipating a significant liquidity event in the next 5 to 7 years, such as the sale of a business or a deferred bonus payout. Their primary concern is not the underlying investments, but how best to manage the tax timing around future withdrawals.

An offshore bond enables the investor to house a diversified portfolio without generating annual tax liabilities and, crucially, allows the gain to be realised at a point when the client’s overall income profile is materially lower. The 5% withdrawal allowance can also be used tactically to supplement income without triggering immediate tax, giving the investor more latitude when structuring a phased retirement or medium-term wealth transfer.

For insurers, this type of planning scenario underscores the importance of efficient unit-linked structures, robust governance and responsive administration, all areas where Guernsey continues to excel.

BWCI

BWCI’s Insurance Management and Insurance Consulting teams have decades of experience in managing unit-linked insurance companies. Our specialists guide clients through Guernsey’s regulatory process, from product design and governance to regulatory reporting, and anti-money laundering. This practical experience helps new companies reach the market quickly and efficiently and help keep them on track.